Businesses operating in Africa increasingly worry about the unpredictable business environment where markets are volatile and political perils are on the rise. This is according to the key findings of the 6th annual Allianz Risk Barometer analyzing corporate risks globally, as well as by region, country, industry, and size of business. Other growing concerns for the businesses, according to the findings are digital dilemmas arising from new technologies and cyber risks as well as natural catastrophes

“Most African countries such as South Africa and Nigeria face macroeconomic challenges including low commodity prices, the Chinese slowdown and the tightening of US monetary policy and also suffer their own internal pressures such as inflation, weak domestic demand, and socio-political tensions,” says Delphine Maïdou, CEO of AGCS Africa.

To mitigate volatility risks and anticipate any sudden changes of rules that could impact markets, companies around the world will need to invest more resources into better monitoring politics and policy-making around the world in 2017. According to trade credit insurer, Euler Hermes, a subsidiary of Allianz SE, since 2014, there have been 600 to 700 new trade barriers introduced globally every year.

Christof Bentele, Head of Global Crisis Management, AGCS says while conventional terrorism is a real concern, the growing risk of political violence events such as war, civil war, insurrection and other politically motivated incidents which focus on countries – particularly in the Middle East and Africa – rather than certain locations should not be underestimated. “The impact for globally operating businesses and our customers can be much greater and longer-lasting,” he says.

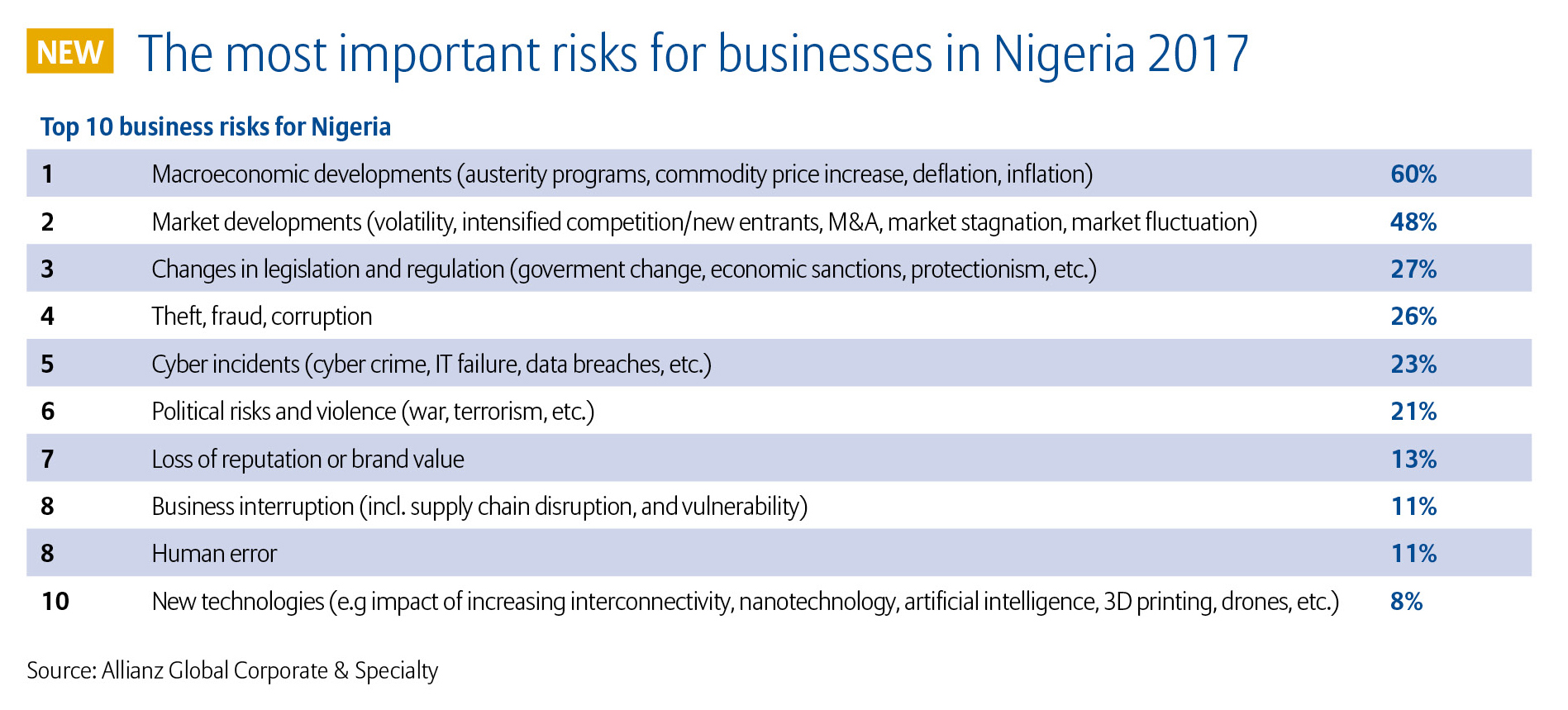

“Instability in African states such as Burundi, The Gambia, Democratic Republic of Congo, Libya, Somalia and South Sudan is a chief concern as well as the persistent Islamic terrorism of Boko Haram in some parts of Nigeria,” adds Bentele.

Globally, business interruption (BI) continues to lead the ranking for the fifth year in a row, primarily because it can lead to significant income losses, but also because multiple new triggers are emerging, especially non-physical damage or intangible perils, such as cyber incidents, and disruption caused by political violence, strikes, and terror attacks. This trend is driven, in part, by the rise of the “Internet of Things” (IoT) and the ever-greater interconnectivity of machines, companies and their supply chains which can easily multiply losses in case of an incident. Companies are also facing potential financial losses with the changing political landscape leading to fears of increasing protectionism and anti-globalization.

“Companies worldwide are bracing for a year of uncertainty,” says Chris Fischer Hirs, CEO of Allianz Global Corporate & Specialty (AGCS) SE. “Unpredictable changes in the legal, geopolitical and market environment around the world are constant items on the agenda of risk managers and the C-suite. A range of new risks are emerging beyond the perennial perils of fire and natural catastrophes which require re-thinking of current monitoring and risk management tools.”

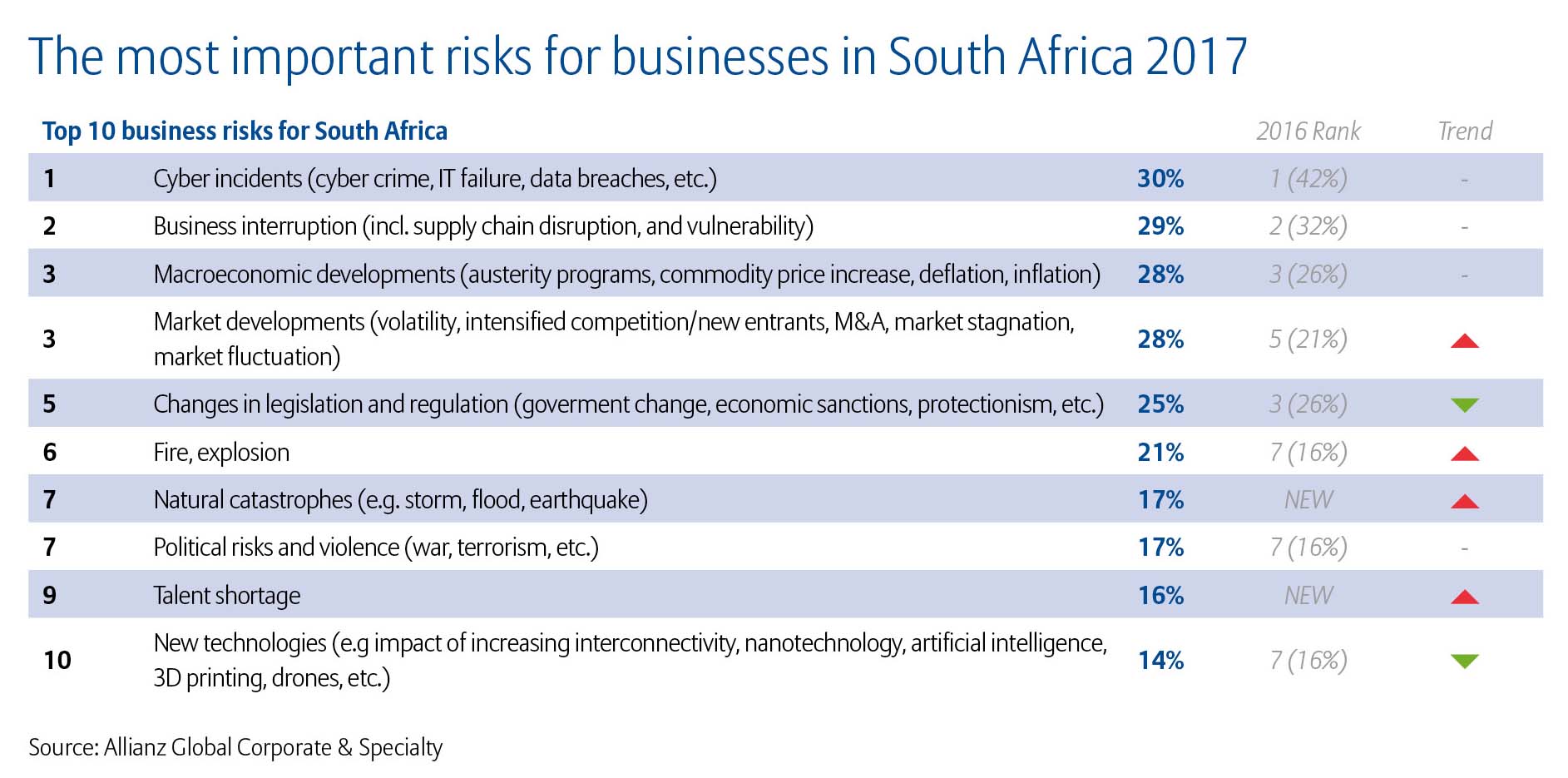

At the same time, increasing reliance on technology and automation is transforming, and disrupting, companies across all industry sectors. While digitalization is bringing companies new opportunities, it is also shifting the nature of corporate assets from mostly physical to increasingly intangible, bearing new hazards, above all cyber risks (30% of responses). Companies ranked cyber threats a close number 3 globally, climbing to position 2 across the Americas and Europe and the top risk in Germany, the Netherlands, South Africa and the UK. At the same time, it is the top concern globally for businesses in the information and telecommunications technology and the retail/wholesale sectors.

“Cyber incidents is ranked number 5 in Africa with the most common threats being from hackers, disgruntled employees, negligence and competitors,” says Nobuhle Nkosi Head of Financial Lines AGCS Africa. “This is a doubled-edged sword to the continent as Africa has a particular role in embracing and responding to new technologies compared to mature markets while speeding up cyber security and personal data protection legislations.”

The threat now goes far beyond hacking and privacy and data breaches, although new data protection regulations will exacerbate the fall-out from these for businesses. Time is running out for businesses to prepare for the implementation of the new General Data Protection Regulation across Europe in 2018 – although the cost of compliance will be high, the penalties for not doing so could be even higher. Meanwhile, increasing interconnectivity and sophistication of cyber-attacks poses not only a huge direct risk for companies but also indirectly via exposed critical infrastructures such as IT, water or power supply. Then there is the threat posed by technical failure or human error, which can lead to long-lasting and widespread BI exposures. In the digitalized production or Industry 4.0 environment, a failure to submit or interpret data correctly could stop production. Businesses need to think about data as an asset and what prevents it from being used.

Results also show that smaller companies may be underestimating cyber risk: in this category (revenues <€250 million), cyber ranks only at number 6. However, the impact of a serious incident could be much more damaging for such firms.

{kind=link}

{kind=link}