For many people across Southern Africa, financial life already runs through a phone screen. Messages arrive. Payments get discussed. Remittances move between relatives and trading partners. The banking step often sits awkwardly outside that rhythm, buried in apps that require data, storage space, and some patience.

A new partnership between Paymentology and Chikwama Pay pushes that friction point out of the way. The plan is simple on the surface. Banking inside WhatsApp.

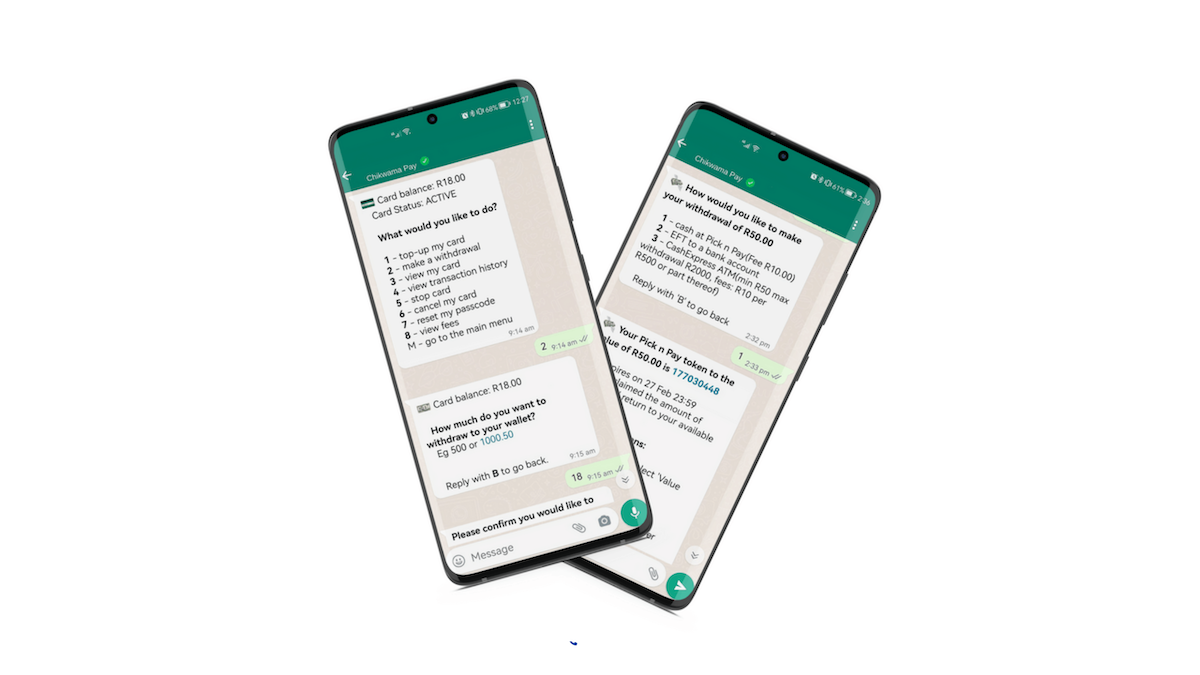

The companies say the arrangement powers what they describe as Africa’s first neo-bank built directly inside the messaging platform. Customers interact with their accounts through the same chat interface they already use to talk with family, organise transport, or negotiate a market price.

The ambition sits inside a familiar African fintech instinct. Work with the tools people already use instead of persuading them to download something new.

A platform already woven into daily life

The choice of WhatsApp is not accidental. Across the continent the app has become infrastructure in its own right, a communication layer sitting underneath commerce, politics, family life, and informal work.

Traders use it to confirm deliveries. Migrant workers rely on it to coordinate remittances home. Community groups organise around it. Many small businesses effectively run their customer support through chat threads.

That existing behaviour has tempted fintech firms for years. Yet turning a messaging service into a reliable financial channel carries complications. Compliance rules differ across countries. Payment processing requires strong fraud controls. Card issuing needs stable infrastructure.

This is where Paymentology enters the story. The London-founded payments processor provides the back-end machinery that allows digital banks to issue and manage debit cards, process transactions, and track activity in real time.

Its technology runs through cloud infrastructure rather than physical processing centres. The model allows financial services to launch across several markets without rebuilding the technical stack for each one.

For a cross-border product, that matters.

Southern Africa’s migrant corridors

Southern African Development Community, often shortened to SADC, brings together 16 member states. The region carries deep economic ties that stretch across borders.

Workers from Zimbabwe often travel to South Africa. Malawian labour flows through farms and mines in neighbouring economies. Informal trade routes connect Zambia, Tanzania, Mozambique and the Democratic Republic of Congo. Small traders carry goods by bus or truck and settle accounts in cash.

Money moves constantly along those corridors. The channels remain fragmented.

Traditional banks often require documentation that migrant workers do not always have. Cross-border transfers can involve fees that eat heavily into small payments. Many people simply hand cash to a bus driver heading in the right direction and trust the money will arrive.

That environment has produced a steady stream of fintech experiments aimed at remittances and mobile wallets.

The idea behind WhatsApp banking in Africa tries to meet that landscape where it already operates. If someone can send a voice note or message through WhatsApp, the platform assumes they can also check a balance, request a transfer, or apply for a microloan inside the same conversation.

The long shadow of mobile money

African finance has already experienced one major digital leap. Mobile money systems such as Safaricom’s M-Pesa showed that a phone number could become a financial identity.

That model spread widely through East Africa and parts of West Africa. Southern Africa took a slightly different path. Banks remained stronger in the formal sector while mobile money adoption grew unevenly.

WhatsApp banking in Africa tries to bridge those two worlds.

Instead of building a wallet network from scratch, Chikwama Pay places a bank interface inside a social messaging environment that millions already open several times a day. The user does not need to navigate a new menu structure or remember a different password pattern.

The bank essentially becomes another contact in the chat list.

It sounds simple. Yet the simplicity hides complicated plumbing beneath the screen.

The machinery underneath the chat

Issuing debit cards requires connections to payment networks. Transaction authorisation must happen instantly. Fraud monitoring has to track behaviour patterns in real time. Regulators expect full compliance with local financial rules.

Paymentology’s platform handles those layers. Its infrastructure processes transactions as they occur while allowing features such as spending controls and transaction notifications.

For a digital bank operating across SADC markets, the technical promise lies in scalability. If the service gains traction in one country, expansion into the next becomes more about regulation and partnerships than rebuilding the technology.

That distinction has become central to modern fintech. Infrastructure companies often carry more influence than the consumer brands visible to customers.

A different entry point for financial services

Chikwama Pay frames its approach around people who remain outside formal banking channels. That group includes migrant workers, market traders, and many women who operate businesses informally.

The traditional financial sector rarely fits their circumstances. Income can fluctuate daily. Proof of residence might not exist. Travel across borders complicates identification requirements.

A WhatsApp interface lowers the psychological barrier to entry. Sending a message to initiate a transaction feels less formal than navigating a bank’s mobile application.

There is also a cultural factor. Messaging apps carry a conversational tone. Banking systems historically project authority and distance.

That contrast shapes how people approach financial decisions.

Regulation enters the chat

Financial regulators across Africa have watched the growth of fintech with cautious interest. Innovation attracts investment and broadens access. It also raises questions around consumer protection, fraud, and data governance.

Operating inside WhatsApp introduces additional layers of oversight. The messaging platform belongs to Meta Platforms, which means financial services sit within a broader technology ecosystem not designed originally for banking.

Authorities will likely scrutinise how customer identification works, how transaction records are stored, and how disputes get resolved. Cross-border activity adds further complexity because each jurisdiction maintains its own regulatory expectations.

None of that blocks experimentation. It simply slows the pace.

Fintech firms across the continent have learned to move through regulatory sand rather than sprint over it.

The economics behind borderless banking

The language around borderless finance often sounds grand. Reality tends to revolve around small transactions.

Remittances worth $50 or $100 matter deeply to families receiving them. Yet fees can carve away a noticeable portion of that value. Cross-border payments frequently involve several intermediaries, each collecting a slice.

If WhatsApp banking in Africa manages to reduce those layers, even modest savings could carry weight for millions of users.

The economic opportunity sits in scale rather than individual transaction size. A platform that handles thousands of small transfers daily begins to look like infrastructure.

That prospect explains why payment processors and digital banks continue experimenting with messaging platforms.

Trust remains the real currency

Technology can move money quickly. Trust moves more slowly.

Many people across the region still prefer physical cash. It carries familiarity and certainty. Digital platforms must earn confidence gradually, especially when transactions cross national borders.

Customer support, dispute resolution, and transparency will determine whether chat-based banking becomes routine or remains a niche tool.

The design of the user experience also matters. Financial services inside messaging apps walk a narrow line. Too many automated prompts and the conversation begins to feel mechanical. Too little structure and transactions become confusing.

Somewhere in that middle ground lies the version that might actually work.

Where the experiment leads

The broader fintech landscape across Africa continues to evolve in unpredictable ways. Mobile money created one pathway. Digital banks are testing another. Messaging platforms now enter the frame as potential financial gateways.

Chikwama Pay’s collaboration with Paymentology places a small but intriguing marker in that landscape.

If WhatsApp banking in Africa gathers momentum, the implications stretch beyond convenience. Banking could move further into everyday communication spaces, dissolving the boundary between conversation and commerce.

That possibility raises practical questions about regulation, competition, and data control. It also reflects something simpler. Financial services follow human behaviour. And increasingly, human behaviour lives inside a messaging window.

Go to TECHTRENDSKE.co.ke for more tech and business news from the African continent and across the world.

Follow us on WhatsApp, Telegram, Twitter, and Facebook, or subscribe to our weekly newsletter to ensure you don’t miss out on any future updates. Send tips to editorial@techtrendsmedia.co.ke